Charity Accounting

Differences between charity and business accounting

Unit 1

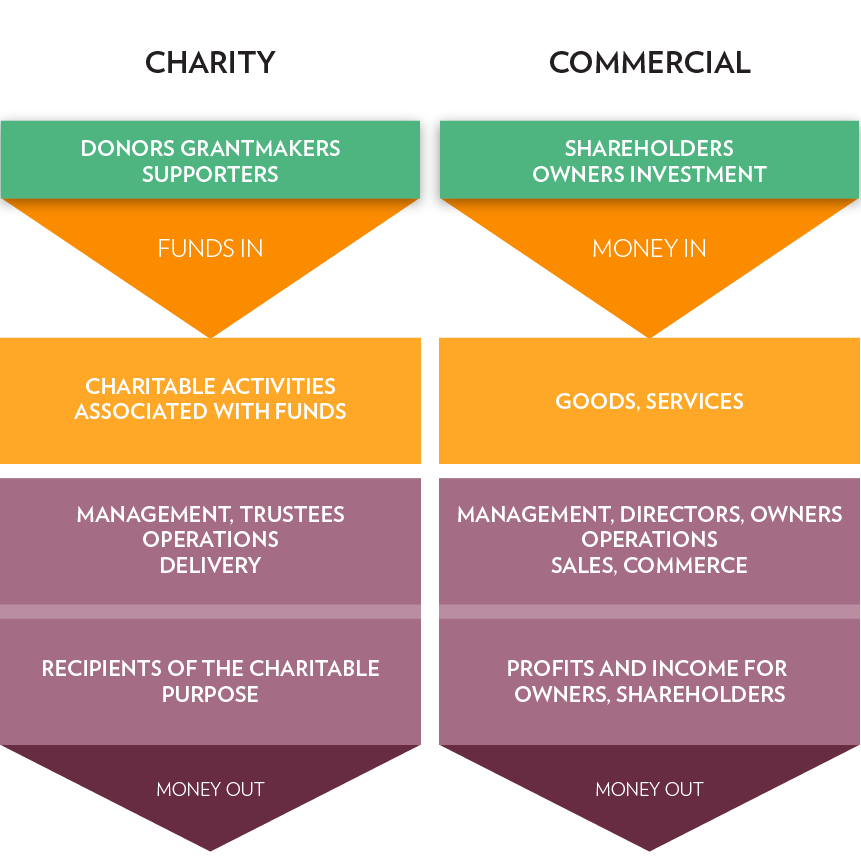

Charity accounting in the UK is designed to demonstrate that the monies given to a charity by supporters are appropriately managed. For commercial enterprises accounting is more for demonstrating the success of the owners/directors in managing the business, providing reassurance for those that trade with it as well as identifying tax liabilities.

Essentially charities are dealing with other people’s money given voluntarily to provide help and support to others, but businesses build income for the owners.

The importance of being able to show that the donations given are used appropriately, and as expected, drive many charity accounting rules.

Fundamental to those accounting rules is the notion of Funds and Fund Accounting. Derived from the requirements of Trust Law in both the legal jurisdictions of England & Wales and Scotland, proper accounting for funds is a legal requirement to prevent a possible breach of trust.

Directly resulting from the critical requirement for proper fund accounting and reporting Regulators recognised that the usual business-type profit and loss presentation fell short of fully explaining all a charity's activities and some years ago introduced the Statement of Financial Activities (SOFA) as the major financial schedule for Charities.

The details of this schedule and other important requirements for charity accounting are laid out in the Charities SORP (Statement of Recommended Practice); which in itself is based upon Financial Reporting Standards (FRS) applicable in the UK and Republic of Ireland that have as key requirement that the accounts provide a “true and fair” view.

Typically commercial activities will use an accounting basis known as Accrual Accounting in which the existence of revenue, assets, expenses and liabilities are recorded in accounting systems when they are known, not necessarily when paid.

Charities (but not charitable companies) that have an income below a certain threshold can chose not to use the accruals basis but a supposedly more simple method known as “Receipts and Payments” consisting of a summary of cash received and paid during the financial period. Unlike the Income and Expenditure basis there is no statutory requirements for Receipts and Payments reporting, although the Charity Authorities offer some guidance notes. As a Receipts and Payments SOFA is not prepared in accordance with accounting standards it does not necessarily offer a 'true and fair' view.

LATEST NEWS

Bank reconciliation is the process of matching the balances in an entity's accounting records to the corresponding information on a bank statement. The goal is to ascertain that the amounts are consistent and accurate, identifying any discrepancies so that they can be resolved.

Understanding UK payroll is essential for businesses, self-employed individuals, and charities. It involves calculating and distributing wages, deducting taxes and contributions, and complying with HMRC regulations. Proper payroll management ensures timely, accurate employee compensation and adherence to tax and employment rules.

The Gift Aid scheme is well known in the charity sector and provides a welcome 25% boost to donation income. There is no limit to how often you can file your claim with HMRC so, if you have processes in place to be able to claim regularly.

Understanding the intricate details of the Church of England's parochial fees can be daunting. These fees, established by the General Synod and Parliament, cover a wide range of church-related services. Here's a deep dive into what these fees entail and how Liberty Accounts can streamline their accounting process for church treasurers.