Profit & loss

Understand the Profit Equation

Unit 4

The Accounting equation provides the basis for an understanding of the financial situation of the business. However over a time period (week, month, year) a business will make a profit or a loss. This is expressed as the Profit Equation:

This equation forms the basis of the second important accounting document known as the PROFIT and LOSS STATEMENT

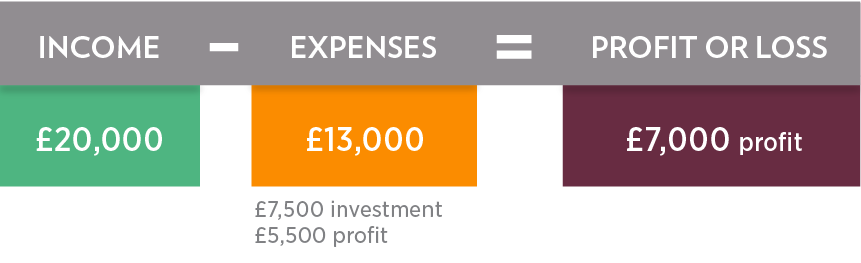

Consider this situation. Business owners have invested £30,000 as cash. They have bought equipment for £15,000 (paying in cash).

During the month the business has bought (on supplier credit) £7,500 worth of raw materials and paid salaries of £5,500.

Goods have been sold for £20,000 (but on credit terms to customers).

The profit equation would look like this:

If this is put together with the accounting equation, we would get the capital increasing by the amount of the profit (£7,000). Liabilities would show what is owed to the supplier (£7,500) and the assets will be made up of the value of the machinery fixed asset (£15,000), the cash balance (£9,500) and the amount owed by the customer (£20,000).

* The cash of £9,500 comes from the £30,000 owners investment less £15,000 spent on machinery and £5,500 on salaries. As yet the customers have not paid and the business has not yet paid suppliers.

The profit equation and accounting equation are clearly linked in that the results of the profit equation over a particular period impact the accounting equation.

Capital changes as a result of profit or loss. The assets (cash) are effected by any sales not yet paid for by customers, likewise liabilities are increased by any suppliers not yet paid.

You may like to try to work through some additional equations, these together with the answers can be down loaded from the link

Further Profit Equation Examples – Adobe PDF format.

The two equations are the essence of bookkeeping and accounting records and will be explored further in future units.

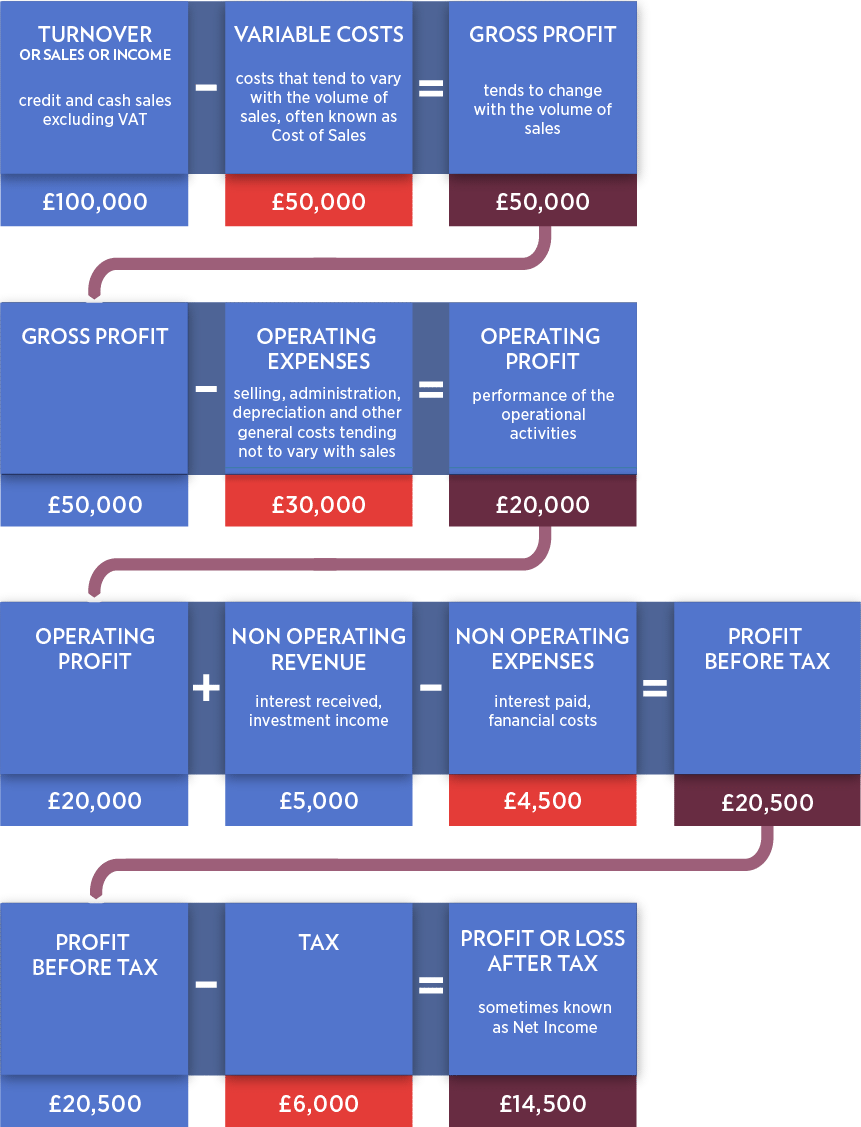

In order to allow a manager to understand how things are going and how the business is performing, the Profit Equation is expanded into a Profit and Loss statement presenting the situation in a lot more detail.

Commonly sales income and expenditure information is recorded in an accounting system into accounts. Each account representing the nature of the income or expenditure. So for example Sales income will be recorded into a sales account and perhaps the expenditure on say renting a building would be recorded into a rent paid account.

The diagram below demonstrates how a usual profit and loss statement is built up.

An important point is that a profit and loss statement will refer to a period of time over which the sales and expenses transactions have occurred. This needs to be shown when a statement is prepared so that a reader understands what the figures refer to.

LATEST NEWS

Bank reconciliation is the process of matching the balances in an entity's accounting records to the corresponding information on a bank statement. The goal is to ascertain that the amounts are consistent and accurate, identifying any discrepancies so that they can be resolved.

Understanding UK payroll is essential for businesses, self-employed individuals, and charities. It involves calculating and distributing wages, deducting taxes and contributions, and complying with HMRC regulations. Proper payroll management ensures timely, accurate employee compensation and adherence to tax and employment rules.

The Gift Aid scheme is well known in the charity sector and provides a welcome 25% boost to donation income. There is no limit to how often you can file your claim with HMRC so, if you have processes in place to be able to claim regularly.

Understanding the intricate details of the Church of England's parochial fees can be daunting. These fees, established by the General Synod and Parliament, cover a wide range of church-related services. Here's a deep dive into what these fees entail and how Liberty Accounts can streamline their accounting process for church treasurers.