Cashflows

Understand how they effect your balance sheet

Unit 7

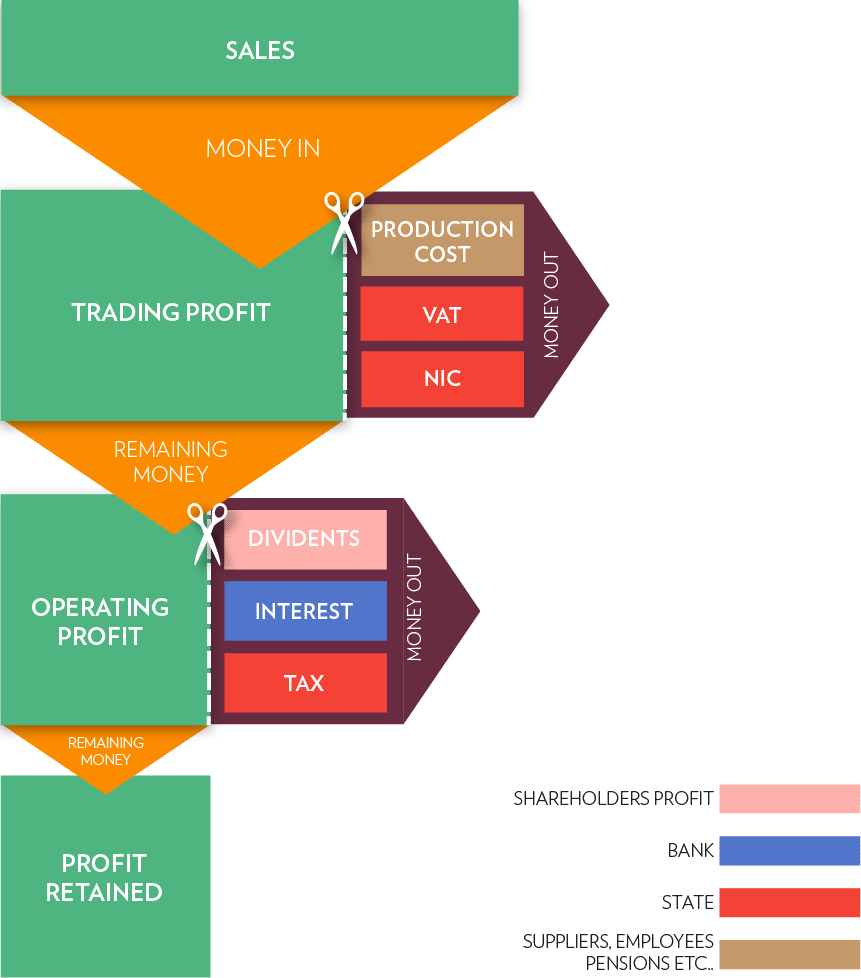

Most business will have trading cash flows as highlighted in the diagram. Cash will come from customers; although not immediately the sale is made if credit is given. Suppliers and employees will take cash from the business, but again there will be a timing factor to take into account. Other regular cash outflows will be interest to lenders of funds, taxation and dividends or drawings to owners.

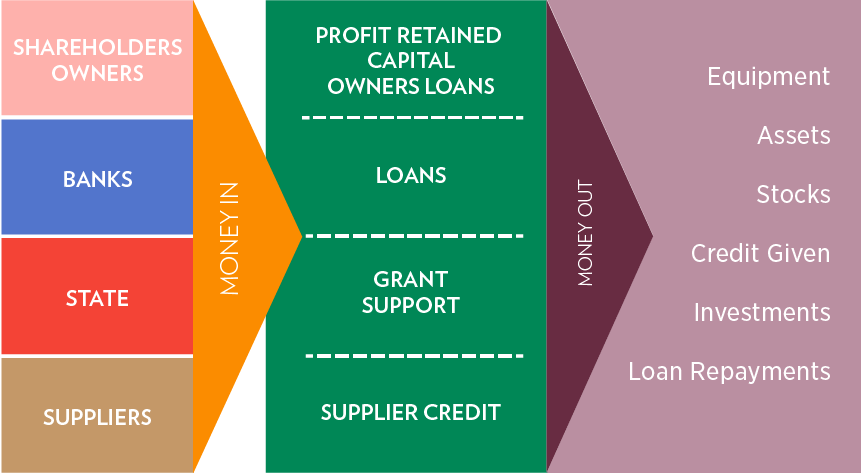

Other cash flows take place when the business purchases equipment, stock, and makes loan repayments as well as the interest.

The business may also decide to make investments which could include investments in other businesses.

The credit terms given to customers need to be funded until the customer pays.

Sometimes a business also uses credit from suppliers as a source of funds.

Clearly an important source of funds is the profits from past trading known as retained earnings.

LATEST NEWS

Bank reconciliation is the process of matching the balances in an entity's accounting records to the corresponding information on a bank statement. The goal is to ascertain that the amounts are consistent and accurate, identifying any discrepancies so that they can be resolved.

Understanding UK payroll is essential for businesses, self-employed individuals, and charities. It involves calculating and distributing wages, deducting taxes and contributions, and complying with HMRC regulations. Proper payroll management ensures timely, accurate employee compensation and adherence to tax and employment rules.

The Gift Aid scheme is well known in the charity sector and provides a welcome 25% boost to donation income. There is no limit to how often you can file your claim with HMRC so, if you have processes in place to be able to claim regularly.

Understanding the intricate details of the Church of England's parochial fees can be daunting. These fees, established by the General Synod and Parliament, cover a wide range of church-related services. Here's a deep dive into what these fees entail and how Liberty Accounts can streamline their accounting process for church treasurers.